Venture capital is a world where dreams are made and shattered equally. While the promise of the next unicorn lures many, the harsh reality is that nine out of ten startups fail!

Just imagine the scale of these losses when billions are at stake. It’s a high-stakes game where many have failed big!

Let’s dive into some of the biggest recent failures in the VC world and see what went wrong.

The harsh reality of venture capital investment

Venture capital is not for the faint of heart. The failure rates are staggering, with over 86% of startups in Europe failing and less than 0.1% achieving an IPO. Around 10% of these startups fail within the first year!

Given these odds, it's no surprise that VC firms are extremely selective. They employ a rigorous vetting process, investing in only about 0.05% of startups. This caution and selectivity stem from the high risk of failure that requires VCs to be meticulous in identifying ventures with the highest potential for success.

But despite all the efforts, significant failures still occur!

Significant VC failures

Let’s examine some notable VC failures over the recent years.

Klarna's Valuation Plunge

Klarna has long been considered a symbol of European startup success. Founded in 2005 in a modest back office in Stockholm by three young postgraduates, the payments and shopping services company quickly gained traction.

By 2010, it had secured funding from US VC heavyweight Sequoia. By March 2021, Klarna had raised $1 billion and was valued at $31 billion, making it Europe’s most valuable startup. Just three months later, another funding round brought in an additional $639 million. That boosted the company’s valuation to $45.6 billion, making it the world’s second most valuable fintech after Stripe.

But the tide quickly changed for the buy now, pay later giant.

By July 2022, Klarna's valuation had plummeted to $6.7 billion — an 85% drop from a year earlier!

Several factors contributed to this dramatic downfall. First, the company’s rapid expansion and aggressive growth strategy led to mounting losses. Despite its revenue growing by 40% to $1 billion in 2020, Klarna’s net losses also increased by 50% due to expansion costs. The company’s net losses were around $109 million in 2020, reflecting the challenges of scaling rapidly while trying to maintain profitability.

The broader economic environment played a critical role as well.

The global market downturn spurred by rising interest rates and inflation significantly affected consumer spending and investor sentiment. As a fintech company heavily reliant on consumer transactions, Klarna's business model also faced increased scrutiny. The layoff of 10% of its workforce in May 2022 was a direct response to these market constraints.

Finally, Klarna's down round in July 2022, where it raised $800 million at a slashed valuation, highlighted the volatility of investor sentiment. Existing investors, like Sequoia, Bestseller, and Silver Lake participated along with new investors like Mubadala, the UAE’s sovereign wealth fund. The belief in Klarna’s long-term potential was still strong.

Klarna’s story underscores the precarious balance VCs must maintain between ambitious growth and sustainable business practices. It also serves as a cautionary tale of how quickly market conditions can shift to turn even the most promising startups into financial liabilities.

The fall of CommonBond

CommonBond was once hailed as a rising star in the fintech space. Founded in 2011 by Wharton MBAs, the company aimed to refinance student loans at lower interest rates to achieve rapid growth and success. By 2019, CommonBond had raised over $1.3 billion in equity and debt funding, reaching a valuation of over $1 billion during a period of profitability.

In September 2022, however, the company announced it would cease operations in what was a dramatic end to a seemingly unstoppable fintech force.

Multiple factors contributed to CommonBond's downfall. First, the federal student loan payment freezes during the COVID-19 pandemic severely contracted its target market. With fewer borrowers seeking refinancing, CommonBond's core business was significantly impacted. Rising interest rates decreased borrower demand and increased customer acquisition costs, further straining the company’s financials.

The competitive landscape around CommonBond also intensified, with traditional lenders and new fintech entrants vying for market share. The heightened competition put additional pressure on CommonBond’s margins and growth prospects. Shrinking capital markets made it further challenging to fund new loan volumes.

CommonBond's fall highlights crucial learning opportunities for founders and investors. The company’s inability to adapt to policy changes, market shifts, and competitive pressures reinforces the need for hindsight, agility, and resilience in business strategies. Even the most promising startups can face rapid reversals if they’re unprepared for turbulent times.

Babylon Health bankruptcy

Babylon Health aimed to revolutionize the digital healthcare industry with its innovative approach combining AI-powered diagnoses and video appointments. The company's vision was to make high-quality healthcare accessible and affordable globally. It gained significant traction to reach a valuation of €4 billion by June 2021, when it went public.

Babylon Health encountered multiple issues that led to its downfall.

- Patient safety and governance issues: Concerns arose about the company's practices regarding patient safety and corporate governance. Despite the innovative use of AI in healthcare, criticisms over the accuracy and reliability of its diagnostic tools began to surface, along with concerns about the overall governance within the company.

- Financial struggles and losses: Babylon's financial performance started to show cracks as it expanded. By 2022, the company reported a net loss of €209.95 million on revenues of €950 million. The financial losses were a significant hit, considering the company's high valuation and the expectations tied to its performance.

- Market and competitive pressures: Babylon faced stiff competition and a challenging regulatory environment as it tried to expand, especially in the US market. The global demand for remote health services was rising, but so were the expectations and the competition from established healthcare providers and other digital health startups.

- Bankruptcy and asset sale: With mounting debt and shrinking cash reserves, Babylon Health found itself in a precarious situation that eventually led to bankruptcy in 2023. The company was eventually sold for a surprisingly low €620,000! The sale to eMed Healthcare UK involved the majority of what was left of Babylon Health, including its preventative telehealth practice.

Babylon Health’s downfall highlights the importance of robust governance, the ability to adapt to competitive pressures, and the need for a sustainable business model. It serves as a stark reminder that even with innovative ideas and significant backing, the execution and management of a startup are what truly determine its success or failure.

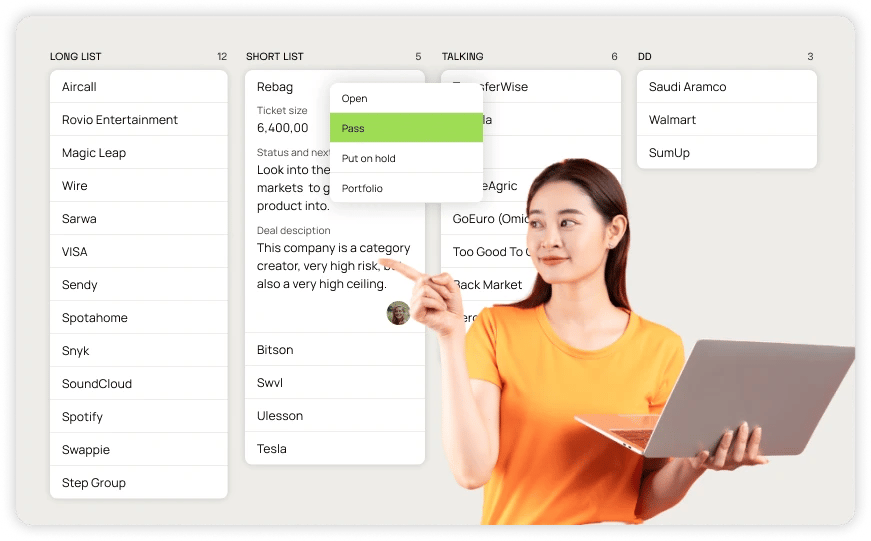

Zapflow - Get more done in less time

So far, we've seen how tough the game can be.

VCs must stay vigilant at all times and manage their operations efficiently to focus on assisting their portfolio companies with all available resources.

That is where we come in! Zapflow is a game changer for investing teams that offers an all-inclusive and easily configurable platform designed for Private Equity, Venture Capital, Family Offices, and Corporate VCs. The platform streamlines processes from deal flow management to LP reporting by consolidating all information into a single, trustworthy source.

Zapflow enables your teams to maximize efficiency and dedicate more time to nurturing valuable relationships.

Schedule a demo today and see how Zapflow can transform your investing process!

Get in touch today!